Owning a home in the beautiful Willamette Valley is a significant achievement, but the financial strategy behind homeownership doesn’t end at the closing table. As market conditions shift and your personal financial situation evolves, the mortgage you signed years ago might no longer be the best fit for your needs. One of the most common questions we hear at Mortgage Marketplace LLC is: “When should I refinance my mortgage?”

Refinancing is a powerful financial tool that can save you thousands of dollars in interest, lower your monthly payments, or provide the cash needed for major life expenses. However, it isn’t a one-size-fits-all solution. Determining the right time to refinance requires a careful look at current interest rates, your home equity, and your long-term goals.

In this guide, we will break down the key indicators that suggest it’s time to refinance, how to calculate your break-even point, and why working with a local Salem, OR mortgage expert like Mike Gillett can ensure you get the best terms possible.

The Top Reasons to Consider Refinancing Now

Refinancing involves replacing your existing mortgage with a new one. While the concept is simple, the reasons for doing so can vary. Here are the most strategic times to consider making the move.

1. Securing a Lower Interest Rate

The most popular reason to refinance is to capitalize on lower interest rates. If market rates have dropped since you purchased your home, refinancing could significantly reduce your monthly payment. Historically, the rule of thumb was that you needed a rate drop of at least 1% to make refinancing worth it. However, with modern loan products and varying closing costs, even a 0.5% reduction can sometimes yield substantial savings over the life of the loan.

If you are currently paying a higher rate, checking today’s rates is the first step to seeing how much you could save.

2. Shortening Your Loan Term

Did you start with a 30-year fixed-rate mortgage but now find yourself in a stronger financial position? Refinancing into a 15-year fixed-rate mortgage can be a game-changer. While your monthly payments might increase slightly (or stay the same if rates have dropped enough), the interest savings over the life of the loan can be massive. You will build equity much faster and own your home free and clear sooner.

3. Accessing Your Home’s Equity (Cash-Out Refinance)

Home values in Salem, OR, and the surrounding areas have seen growth over recent years. If your home is worth more than you owe, you have “equity.” A cash-out refinance allows you to tap into that wealth by taking out a new loan for more than your current balance and receiving the difference in cash.

Homeowners often use this strategy for:

- Home Improvements: Reinvesting in the property to increase its value further (e.g., a kitchen remodel or adding an ADU).

- Debt Consolidation: Paying off high-interest credit cards or personal loans using the lower interest rate of a mortgage.

- Education Expenses: Funding college tuition.

To see how this might look for your specific situation, you can use our Refinance Analysis tool.

4. Eliminating Private Mortgage Insurance (PMI)

If you purchased your home with less than 20% down—perhaps using an FHA loan or a conventional loan with low down payment options—you are likely paying for Private Mortgage Insurance (PMI). This insurance protects the lender, not you, and it adds to your monthly costs.

If your home’s value has increased and your loan balance has decreased enough to give you 20% equity, refinancing into a conventional loan can eliminate that PMI payment, instantly lowering your monthly overhead.

5. Switching from an Adjustable-Rate to a Fixed-Rate Mortgage

Adjustable-Rate Mortgages (ARMs) often start with a lower introductory rate, but they carry the risk of rising payments once the adjustment period begins. If you are currently in an ARM and rates are rising, refinancing into a 30-year fixed-rate mortgage provides stability. You will lock in a consistent principal and interest payment for the life of the loan, protecting you from future market volatility.

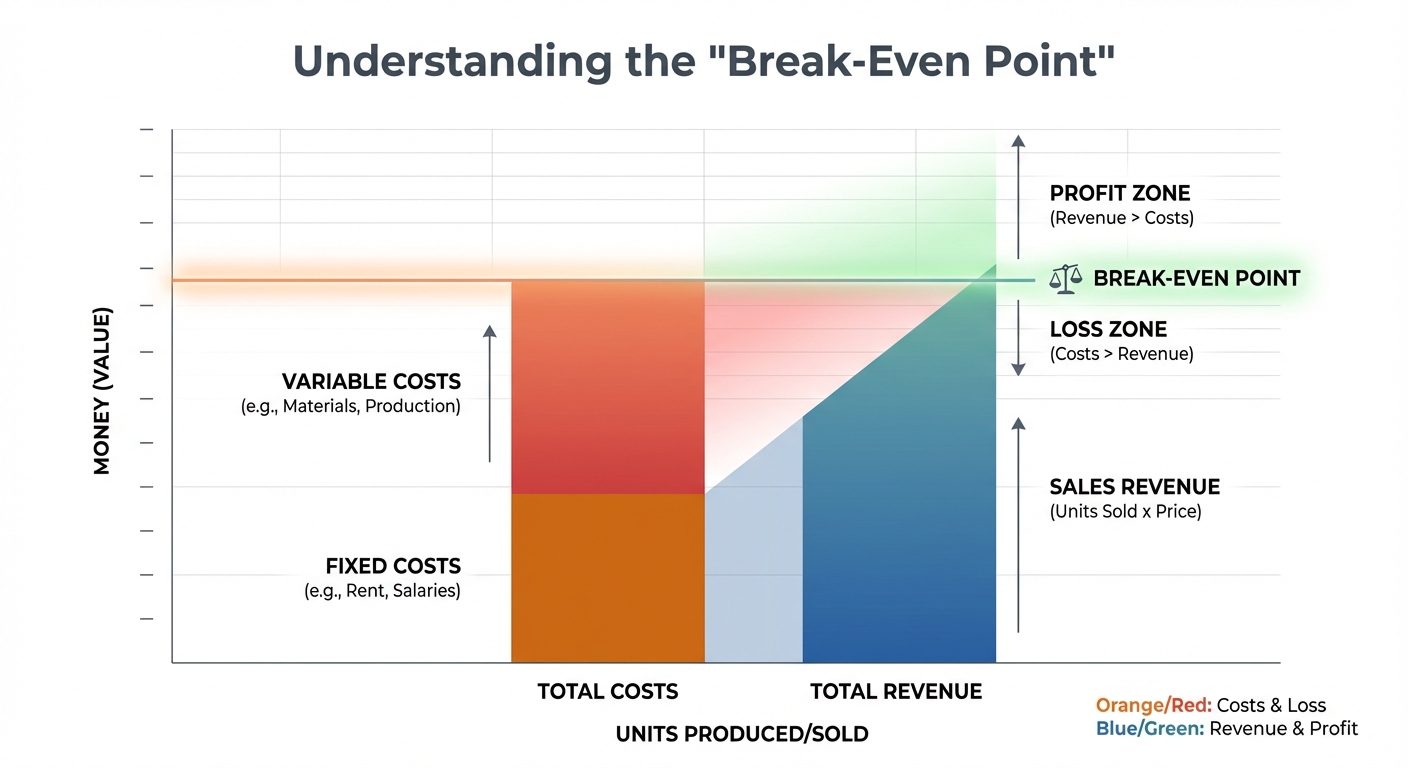

Understanding the “Break-Even Point”

The Calculation:

Total Closing Costs ÷ Monthly Savings = Months to Break Even

For example, if your refinance costs $4,000 to close, but it saves you $200 per month on your mortgage payment, your break-even point is 20 months ($4,000 ÷ $200). If you plan to stay in your Salem home for longer than 20 months, the refinance is a sound financial decision. If you plan to move in a year, it would not make financial sense.

Local Spotlight: Refinancing in Salem, OR

Real estate is hyper-local, and so is mortgage lending. While national headlines give a broad overview, the conditions in Oregon can differ. Working with a local expert like Mortgage Marketplace LLC offers distinct advantages over big-box online lenders.

- Accurate Appraisals: We understand the unique value of properties in neighborhoods throughout Salem, Keizer, and the Willamette Valley. This ensures your appraisal accurately reflects your home’s worth, which is critical for removing PMI or maximizing a cash-out refinance.

- Speed and Efficiency: Our team is based locally at 3723 Fairview Industrial Dr. SE. We have relationships with local title companies and appraisers, which often allows us to close loans faster—sometimes fully funded in 30 days or less.

- Personalized Service: You aren’t just a loan number. Whether you call Mike Gillett or any member of our team, you get direct access to an advisor who knows your financial history and goals.

Comparison: Current Loan vs. Refinance Scenarios

| Scenario | Loan Balance | Interest Rate | Term Remaining | Monthly P&I Payment | Total Interest Paid (Remaining) |

|---|---|---|---|---|---|

| Current Loan | $350,000 | 6.5% | 28 Years | $2,212 | $393,000 |

| Refinance (Rate & Term) | $350,000 | 5.5% | 30 Years | $1,987 | $365,000 |

| Refinance (15-Year) | $350,000 | 5.0% | 15 Years | $2,767 | $148,000 |

*Note: These figures are for educational purposes only. Rates fluctuate daily. To get numbers based on your specific scenario, please contact us for a personalized quote.

The Refinance Process with Mortgage Marketplace

We strive to make the process as seamless as possible. Here is what you can expect when you choose to refinance with us:

- Initial Consultation: We discuss your goals (lower payment, cash out, etc.) and review your current mortgage details.

- Application & Pre-Approval: You complete a streamlined online application. We review your credit and income to provide loan options.

- Rate Lock: Once you choose a loan program, we lock in your interest rate to protect you from market fluctuations.

- Processing & Underwriting: We verify your documents and order an appraisal (if required). Our team handles the heavy lifting here.

- Closing: You sign the final documents. For a refinance, there is typically a 3-day “right of rescission” period before the loan funds.

Frequently Asked Questions (FAQs)

1. How often can I refinance my home?

2. Will refinancing hurt my credit score?

Initially, you may see a small dip in your credit score due to the “hard inquiry” when lenders check your credit report. However, this is usually temporary. In the long run, if refinancing lowers your monthly debt payments or helps you consolidate high-interest debt, it can actually improve your credit utilization ratio and boost your score.

3. Can I refinance with bad credit?

Yes, options exist. While conventional loans generally require higher credit scores, FHA refinances and VA Interest Rate Reduction Refinance Loans (IRRRL) have more flexible credit requirements. If your credit has improved since you bought your home, you might qualify for better terms than you currently have.

4. What are “no-closing-cost” refinances?

A “no-closing-cost” refinance doesn’t mean the fees disappear. Instead, the lender usually covers the closing costs in exchange for a slightly higher interest rate, or the costs are rolled into the principal balance of the loan. This can be a good strategy if you are short on cash upfront but want to lower your monthly payment immediately.

5. What documents do I need to refinance?

Generally, the documentation is similar to when you bought your home. You will likely need:

- Recent pay stubs (last 30 days).

- W-2 forms (last 2 years).

- Bank statements (last 2 months).

- Proof of homeowners insurance.

- Current mortgage statement.

Ready to Explore Your Refinance Options?

Deciding when to refinance is a major financial move, but you don’t have to make the decision alone. At Mortgage Marketplace LLC, we specialize in helping homeowners in Salem, Oregon, and beyond evaluate their options with honesty and integrity. Whether you want to slash your monthly payment, pay off your home sooner, or get cash out for a renovation, we are here to crunch the numbers for you.

Don’t leave money on the table. Mortgage rates change daily, and locking in at the right time is key.

Contact Mike Gillett and the team today:

- Call or Text: (503) 510-8780

- Email: mike.gillett@p9t630biym.wpdns.site

- Office: 3723 Fairview Industrial Dr. SE, Suite 190, Salem, OR 97302

Get Your Free Refinance Analysis Now

Mortgage Marketplace LLC

NMLS #2367229 | Mike Gillett NMLS #362285

3723 Fairview Industrial Dr. SE, Suite 190, Salem, OR 97302

Phone: (503) 210-1480

Equal Housing Opportunity. This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements for refinances, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines.