")

Why Salem Homeowners Are Leveraging Equity Extraction in 2026

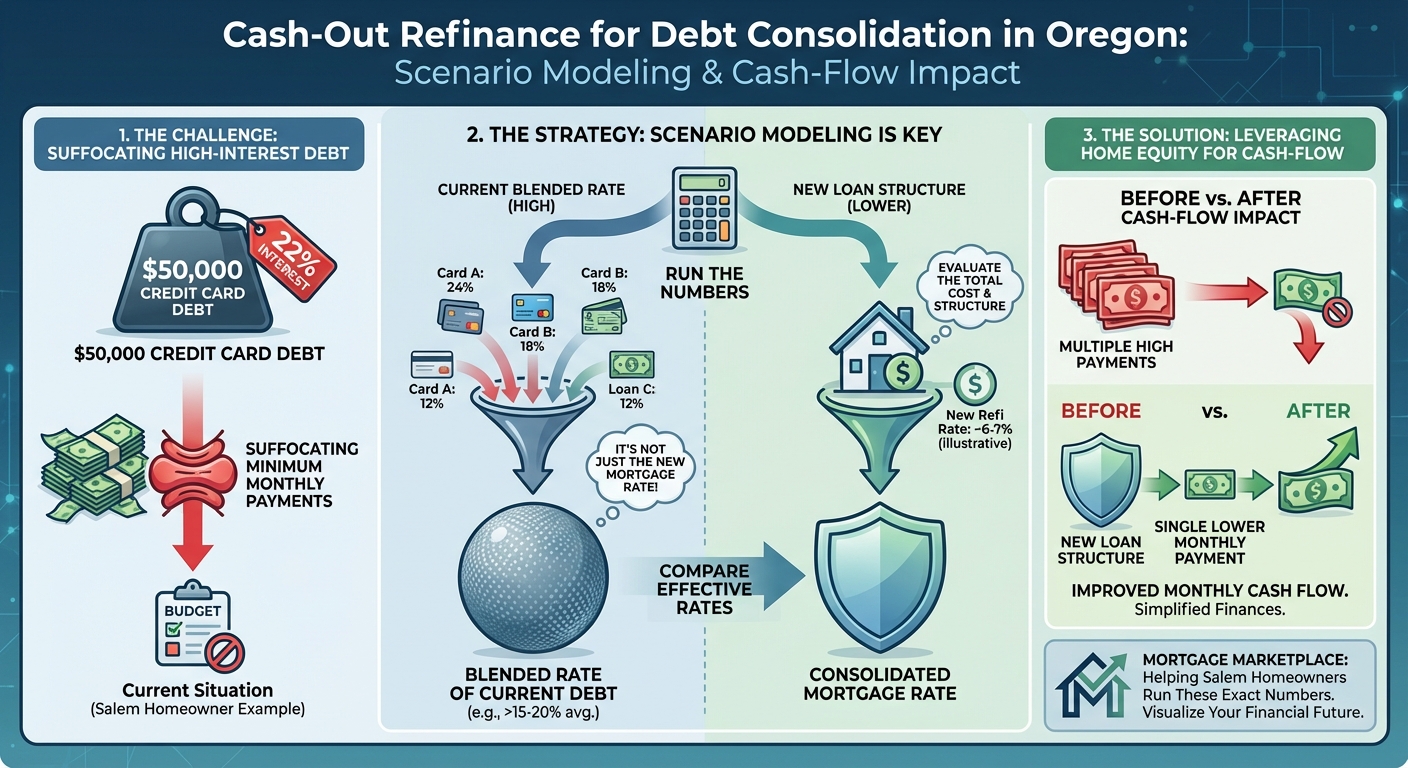

As we navigate the economic landscape of 2026, homeowners in Salem, OR, and throughout the Pacific Northwest are discovering the strategic power of a cash-out refinance. With property values maintaining strong positions, equity extraction has become a primary tool for savvy financial planning. But when does tapping into your home equity actually deliver long-term value?

Debt consolidation remains one of the most compelling reasons to consider a cash-out refinance. By rolling high-interest credit card debt or personal loans into a single, lower-interest mortgage payment, you can significantly improve your monthly cash flow. Working with a local expert like Mike Gillett at Mortgage Marketplace LLC ensures you are not just chasing a lower rate, but strategically managing your debt to support your broader financial goals.

- Improved Cash Flow: Consolidating multiple high-interest debts into one predictable monthly payment.

- Potential Tax Benefits: Understanding the nuances of mortgage interest deductibility for home improvements versus debt consolidation.

- Strategic Debt Management: Shifting unsecured, variable-rate debt into a stable, long-term fixed asset.

Before proceeding, it is crucial to model different scenarios. A well-structured refinance should align with your long-term wealth-building strategy, not just provide a short-term cash injection.

Scenario Modeling: Cash-Flow Impact and Interest Deductibility

When exploring a cash-out refinance for debt consolidation in Oregon, scenario modeling is your best friend. It is not enough to simply look at the new mortgage rate. You must evaluate the blended rate of your current debt compared to the new loan structure. At Mortgage Marketplace, we help Salem homeowners run these exact numbers.

Consider the cash-flow impact. If you have $50,000 in credit card debt at 22% interest, your minimum monthly payments are likely suffocating your budget. By leveraging a cash-out refinance, you might increase your mortgage balance, but the overall monthly outlay drops dramatically. This freed-up capital can be redirected into retirement savings, college funds, or property upgrades.

Important Compliance Note: Tax laws regarding mortgage interest deductibility are complex. Generally, interest on a cash-out refinance is only deductible if the funds are used to buy, build, or substantially improve the taxpayer’s home that secures the loan. Funds used for debt consolidation typically do not qualify for this deduction. Always consult with a licensed tax professional in Oregon to understand your specific tax situation. Mortgage Marketplace LLC is an Equal Housing Lender providing financing solutions, not tax advice.

| Debt Type | Current Balance | Current Interest Rate | Estimated Monthly Payment |

|---|---|---|---|

| Credit Cards | $35,000 | 24.5% | $1,050 |

| Auto Loan | $25,000 | 8.5% | $520 |

| Personal Loan | $15,000 | 12.0% | $340 |

| Total Current Debt | $75,000 | Blended: ~16.5% | $1,910 |

| Cash-Out Refinance | $75,000 (Added to Mortgage) | Current Market Rate | ~$450 to $550 (Varies by Term) |

Making the Right Move with Mortgage Marketplace

Extracting equity requires a clear-eyed view of your financial future. As we look at the Salem, OR housing market in 2026, homeowners have a unique opportunity to restructure their finances. However, converting unsecured debt into secured debt means your home is on the line. It is a powerful strategy, but one that requires discipline and expert guidance.

We compare loan options across multiple lenders to help you access competitive rates and flexible loan structures. Whether you are looking at a 30-Year Fixed Rate Mortgage or exploring alternative home loan options, our goal is to provide a side-by-side rate comparison. This transparency reveals meaningful differences in payments, costs, and flexibility.

Ready to see if a cash-out refinance makes sense for your debt consolidation goals? A well-structured plan can protect your home equity while delivering immediate financial relief. Let our team run the scenario modeling for you.

Q1: What is a cash-out refinance and how does it work for debt consolidation?

A cash-out refinance replaces your existing mortgage with a new, larger loan. You receive the difference between the two loans in cash, which you can then use to pay off high-interest debts like credit cards or personal loans, consolidating them into one monthly mortgage payment.

Q2: Are the interest payments on a cash-out refinance for debt consolidation tax-deductible in Oregon?

Generally, no. Under current tax laws, mortgage interest is typically only deductible if the extracted equity is used to buy, build, or substantially improve the home securing the loan. Always consult a tax professional regarding your specific situation.

Q3: How does debt consolidation through refinancing impact my monthly cash flow?

By rolling high-interest, short-term debt into a lower-interest, long-term mortgage, your total monthly debt obligations usually decrease significantly. This improves your monthly cash flow, freeing up money for savings or other expenses.

Q4: Is it risky to use my home equity to pay off credit card debt?

It can be if you do not change the spending habits that led to the credit card debt. You are converting unsecured debt into secured debt, meaning your home is collateral. It is a smart move if paired with disciplined financial management.

Q5: How quickly can I close on a cash-out refinance in Salem, OR?

With complete information and proactive planning, most home loans and refinances at Mortgage Marketplace close in less than 30 days. Our streamlined online process helps avoid common delays.