—

Understanding the Basics of a HELOC

If you are a homeowner in Salem, OR looking to fund a major project, consolidate debt, or cover unexpected expenses, a heloc home equity line of credit might be the perfect financial tool for you.

A HELOC functions much like a credit card. It is a revolving line of credit secured by the equity you have built in your property. Unlike a lump-sum loan, you only borrow what you need and pay interest strictly on the amount you draw. Homeowners frequently compare this option with a home equity loan or second mortgage or consider a cash-out refinance to determine which path best suits their financial goals.

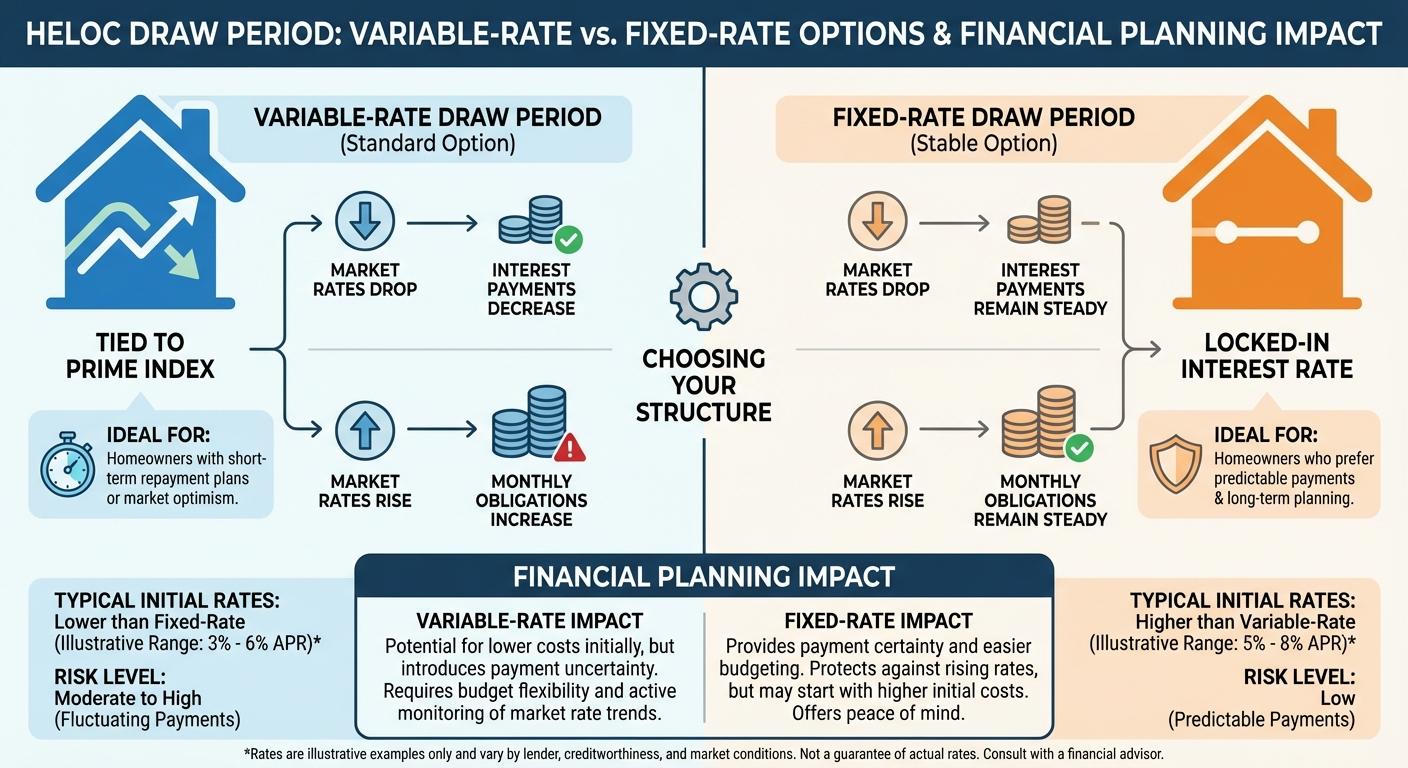

One of the most critical aspects of a HELOC is understanding the draw period. This is the timeframe, typically 10 years, during which you can access your funds. During this phase, you will encounter two primary rate structures:

- Variable-Rate Draw Periods: The interest rate fluctuates based on market conditions, which means your minimum monthly payments can go up or down.

- Fixed-Rate Draw Periods: Some lenders offer the option to lock in a portion of your balance at a fixed interest rate, providing predictable, stable monthly payments.

At Mortgage Marketplace LLC, we are experts at providing second opinions on HELOCs to ensure you secure the most competitive terms available in the local market.

Variable-Rate vs. Fixed-Rate Draw Periods

Choosing between a variable-rate and a fixed-rate draw period is a major decision when setting up your heloc home equity line of credit. Let us break down how each option impacts your financial planning.

A variable-rate structure is the standard for most HELOCs. Because the rate is tied to a prime index, it offers flexibility. If market rates drop, your interest payments decrease. However, if rates rise, your monthly obligations will increase. This option is ideal for homeowners who plan to pay off their balance quickly or those who can comfortably handle payment fluctuations.

Conversely, a fixed-rate option allows you to convert a portion or all of your outstanding variable-rate balance into a fixed loan. This provides immense peace of mind. Knowing exactly what your payment will be each month makes budgeting significantly easier, especially for long-term home renovations in Salem, OR.

| Feature | Variable-Rate HELOC | Fixed-Rate HELOC Option |

|---|---|---|

| Interest Rate | Fluctuates with the market index | Locked in for a specific term |

| Monthly Payment | Can change monthly | Remains consistent and predictable |

| Best For | Short-term borrowing and quick payoffs | Long-term debt consolidation or major renovations |

Why Get a Second Opinion on Your HELOC?

Not all home equity lines of credit are created equal. Lenders have different margin rates, fee structures, and introductory offers. If you have already received a quote from another financial institution, bringing it to Mortgage Marketplace LLC is a smart move. We are experts at providing second opinions on HELOCs.

Our team, led by Mike Gillett, takes pride in helping Salem homeowners navigate their financing options. We compare loan programs across multiple lenders to ensure you are not missing out on a better rate or a more favorable fixed-rate draw period. By reviewing your scenario comprehensively, we often uncover ways to lower your payments or increase your borrowing power.

Whether you are weighing a HELOC against a cash-out refinance or just want to confirm you are getting the best possible deal, our local expertise is at your disposal.

Q1: What is a HELOC home equity line of credit?

A HELOC is a revolving line of credit that allows you to borrow against the equity in your home. You can draw funds as needed and only pay interest on the amount you actually use.

Q2: How does a variable-rate draw period work?

During a variable-rate draw period, your interest rate fluctuates based on a benchmark index. This means your minimum monthly payments can change as market rates rise or fall.

Q3: Can I lock in a fixed rate on my HELOC?

Yes, many lenders offer a fixed-rate option that allows you to convert a portion of your outstanding balance into a fixed-rate loan, providing predictable monthly payments.

Q4: Why should I get a second opinion on a HELOC offer?

Lenders vary widely in their rates, fees, and terms. Getting a second opinion from Mortgage Marketplace LLC ensures you are securing the most competitive and flexible terms available for your unique financial situation.

Q5: Is a HELOC better than a cash-out refinance?

It depends on your current mortgage rate and financial goals. A HELOC allows you to keep your primary mortgage intact, which is highly beneficial if you have a low first mortgage rate, whereas a cash-out refinance replaces your existing mortgage entirely.

Call Mike Gillett at (503) 510-8780 to Get Your HELOC Second Opinion Today!