—

What is an Adjustable-Rate Mortgage (ARM)?

An Adjustable-Rate Mortgage (also known as ARM, 5/1 ARM or 7/1 ARM) is a home loan with an interest rate that can change periodically. This means that your monthly payments can go up or down over time. Generally, the initial interest rate is lower than that of a comparable 30-year fixed-rate mortgage or 15-year fixed-rate mortgage. After the initial fixed period ends, the interest rate adjusts based on a specific financial benchmark.

At Mortgage Marketplace LLC in Salem, OR, we help homebuyers and homeowners navigate their financing options. Whether you are considering a 5/1 ARM, a 7/1 ARM, or a 10/1 ARM, understanding the mechanics of these loans is crucial. The first number represents the number of years the initial interest rate is fixed. The second number indicates how often the rate can adjust after the fixed period. For example, a 5/1 ARM has a fixed rate for five years and then adjusts annually.

We are experts at providing second opinions on adjustable-rate mortgages. If you are unsure whether an ARM is the right fit for your financial goals, Mike Gillett and our local Salem mortgage brokers can review your scenario and compare it against other loan options.

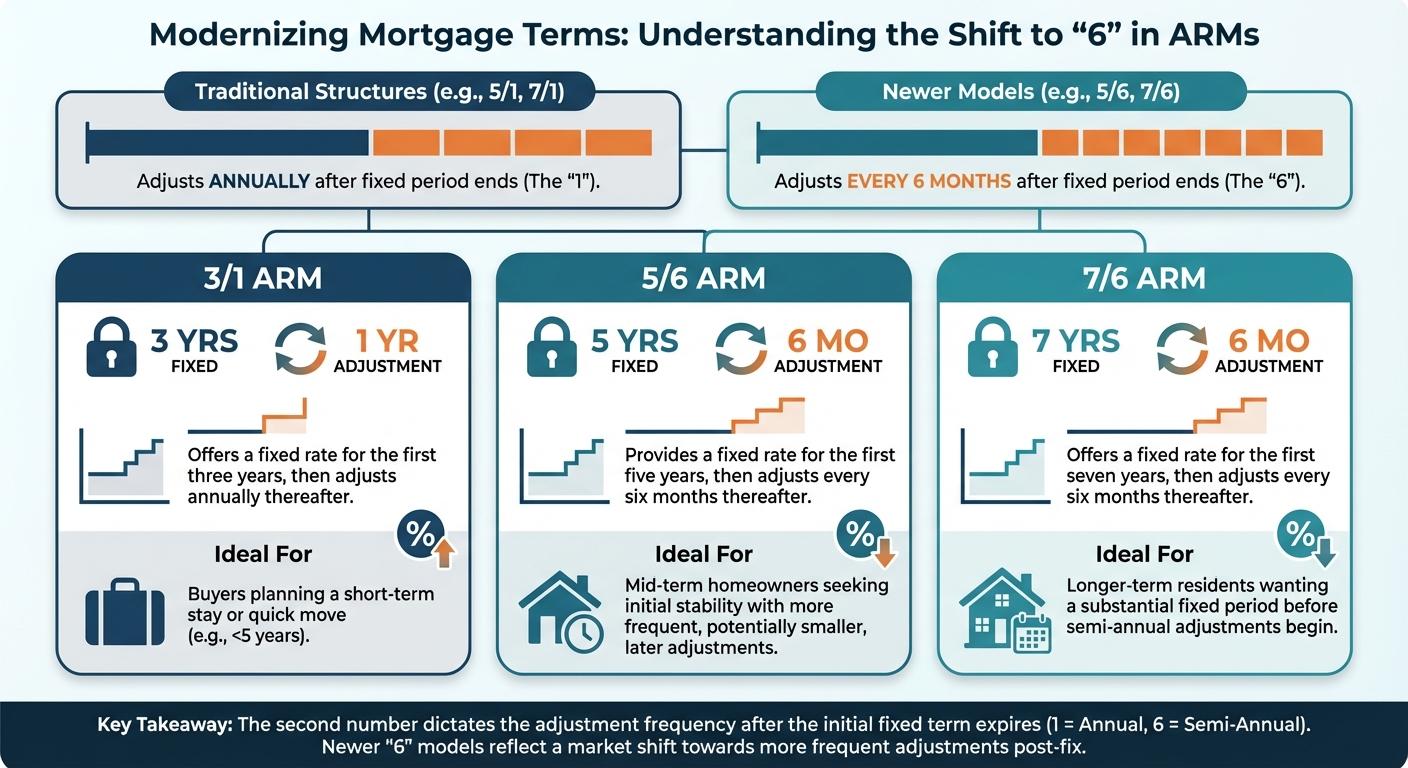

Exploring Different ARM Structures: 3/1, 5/6, 7/6, and 10/1 ARMs

While traditional 5/1 and 7/1 structures are popular, the mortgage industry has introduced updated terms like the 5/6 ARM and 7/6 ARM. In these newer models, the number six means the rate adjusts every six months instead of annually after the fixed period expires. Here is a breakdown of common adjustable-rate mortgage terms:

- 3/1 ARM: Offers a fixed rate for three years, adjusting annually thereafter. Ideal for buyers planning a short-term stay.

- 5/6 ARM and 7/6 ARM: Provide a fixed rate for five or seven years, respectively, and then adjust every six months.

- 10/1 ARM: Secures your rate for a full decade before annual adjustments begin, offering stability similar to fixed loans but often with a slightly lower introductory rate.

When dealing with higher loan amounts, an ARM can be paired with a jumbo mortgage to keep initial monthly payments manageable. However, it is vital to understand caps and floors. Caps limit how much your interest rate can increase during a single adjustment period and over the life of the loan. Floors dictate the lowest possible rate your mortgage can drop to. These protections ensure your payments remain within a predictable range.

| ARM Type | Fixed Rate Period | Adjustment Frequency | Best For |

|---|---|---|---|

| 3/1 ARM | 3 Years | Annually | Short-term homeowners |

| 5/1 ARM | 5 Years | Annually | Medium-term planners |

| 5/6 ARM | 5 Years | Every 6 Months | Buyers expecting to move in 5 years |

| 7/6 ARM | 7 Years | Every 6 Months | Those seeking moderate stability |

| 10/1 ARM | 10 Years | Annually | Long-term residents wanting initial savings |

Is an Adjustable-Rate Mortgage Right for You in Salem?

Deciding on an adjustable-rate mortgage depends heavily on your future plans and current financial situation. If you plan to sell your Salem home or refinance before the fixed-rate period ends, an ARM can save you thousands of dollars in interest. On the other hand, if you plan to stay in your home forever, a fixed-rate loan might offer better peace of mind.

Many homeowners use an ARM to secure a lower initial rate and then utilize a rate and term refinance to switch to a fixed-rate mortgage before the adjustments begin. As your local mortgage broker in Salem, OR, Mortgage Marketplace LLC is here to help you weigh the pros and cons. We pride ourselves on offering comprehensive comparisons across multiple lenders, ensuring you get the best possible terms.

Remember, we are experts at providing second opinions on adjustable-rate mortgages. If another lender has offered you an ARM and you want to verify it is truly competitive, let our team review your offer today.

Q1: What is an adjustable-rate mortgage?

An adjustable-rate mortgage is a home loan where the interest rate remains fixed for an initial period and then adjusts periodically based on market indexes.

Q2: How does a 5/1 ARM work?

A 5/1 ARM features a fixed interest rate for the first five years of the loan. After that initial period, the interest rate adjusts once every year for the remainder of the loan term.

Q3: What are interest rate caps and floors?

Caps are limits placed on how much your interest rate can increase during an adjustment period and over the life of the loan. Floors are the minimum rate your loan can drop to, protecting both you and the lender.

Q4: Should I choose a 5/6 ARM or a traditional fixed-rate mortgage?

A 5/6 ARM is great if you plan to move or refinance within five years, as it typically offers a lower starting rate. A fixed-rate mortgage is better if you plan to stay in your home long-term and prefer predictable monthly payments.

Q5: Can I refinance my ARM before the rate adjusts?

Yes, many borrowers choose a rate and term refinance to transition from an adjustable-rate mortgage into a fixed-rate loan before their initial fixed period ends.

Contact Mike Gillett at Mortgage Marketplace LLC in Salem, OR Today for a Second Opinion on Your ARM