One of the first questions we hear from aspiring homeowners in Salem, Oregon, is simple yet loaded with anxiety: “What credit score do I need to buy a house?”

It is a valid concern. Your credit score is one of the most significant factors lenders use to determine your eligibility for a mortgage and the interest rate you will pay. However, the answer isn’t a single, magic number. The credit score required depends heavily on the type of loan you are applying for, your down payment, and your overall financial picture.

At Mortgage Marketplace LLC, we believe that a number shouldn’t stand between you and your dream home. Whether you have pristine credit or a few bumps in the road, there are likely options available to you. In this comprehensive guide, we will break down the minimum credit score requirements for different loan programs and explain how you can navigate the path to homeownership right here in the Willamette Valley.

The Short Answer: Is There a Minimum Score?

Generally speaking, a credit score of 620 is considered the benchmark for a conventional mortgage. However, you can qualify for government-backed loans (like FHA loans) with scores as low as 580, and in some specific cases, even lower.

It is important to remember that while meeting the minimum score gets your foot in the door, a higher score typically unlocks lower interest rates, which can save you thousands of dollars over the life of your loan. Let’s dive into the specifics of each loan type.

Credit Score Requirements by Loan Type

Different mortgage programs have different risk tolerances. Because some loans are backed by the federal government, lenders can afford to be more lenient with credit requirements. Here is what you need to know about the most common loan options available in Salem and throughout Oregon.

1. Conventional Loans

Typical Minimum Score: 620

A conventional loan is not insured by the federal government. These are usually backed by Fannie Mae or Freddie Mac. Because the lender takes on more risk, the standards are slightly stricter.

- 620+ Credit Score: Most lenders require at least a 620.

- Down Payment: Can be as low as 3% for first-time homebuyers, though 5% to 20% is common.

- Impact of Score: If your score is between 620 and 680, you may pay a higher interest rate and higher Private Mortgage Insurance (PMI) premiums compared to someone with a score of 740+.

2. FHA Loans (Federal Housing Administration)

Typical Minimum Score: 580 (with 3.5% down)

FHA loans are a fantastic option for first-time buyers or those with less-than-perfect credit. The government insures these loans, encouraging lenders to work with a broader range of borrowers.

- 580+ Credit Score: Qualifies you for the low down payment advantage of just 3.5%.

- 500-579 Credit Score: It is technically possible to qualify, but you may be required to put down 10% or more.

- Debt-to-Income (DTI): FHA loans are often more forgiving regarding DTI ratios, sometimes allowing higher ratios than conventional loans.

3. VA Loans (Department of Veterans Affairs)

Typical Minimum Score: 580-620 (Lender discretion)

If you are a veteran, active-duty service member, or eligible surviving spouse, the VA loan is arguably the best mortgage product on the market. Technically, the VA does not set a minimum credit score requirement. However, most lenders (including us) look for a minimum score to ensure the borrower is a good risk.

- No Down Payment: 0% down required.

- No PMI: This saves you a significant amount on monthly payments.

- Flexible Credit: While 620 is a common lender benchmark, exceptions can often be made for borrowers with scores starting around 580 who have strong residual income.

4. USDA Loans (U.S. Department of Agriculture)

Typical Minimum Score: 640

USDA loans are designed to encourage homeownership in rural areas. Many areas just outside of Salem and the greater Marion County area qualify for this program.

- 640+ Credit Score: This is the standard for the USDA’s automated underwriting system.

- 0% Down Payment: Like VA loans, USDA loans allow for 100% financing.

- Income Limits: You must meet income eligibility requirements to qualify.

5. Jumbo Loans

Typical Minimum Score: 700-720

If you are looking to buy a luxury home in Oregon that exceeds conforming loan limits, you will likely need a Jumbo loan. Because these loans involve large amounts of money and are not government-insured, lenders require reassurance.

- High Credit Standards: Expect to need a score of 700 or higher.

- Larger Down Payment: Often requires 10% to 20% down.

- Reserves: Lenders may ask to see proof of 6-12 months of mortgage payments in liquid cash reserves.

Quick Comparison: Credit Score vs. Loan Type

Here is a snapshot of what you generally need to qualify:

| Loan Type | Minimum Credit Score (Typical) | Down Payment Requirement | Best For… |

|---|---|---|---|

| Conventional | 620 | 3% – 20% | Borrowers with good credit and stable income. |

| FHA | 580 | 3.5% | First-time buyers or those with credit bumps. |

| VA | 580 – 620 | 0% | Veterans and active military. |

| USDA | 640 | 0% | Buyers in rural/suburban areas. |

| Jumbo | 700+ | 10% – 20% | High-value property purchases. |

It’s Not Just About the Score: Other Qualifying Factors

While your credit score is the headline, the full story of your mortgage approval involves the “whole borrower” approach. Mike Gillett and the team at Mortgage Marketplace LLC look at several factors to help you get approved, even if your score is on the borderline.

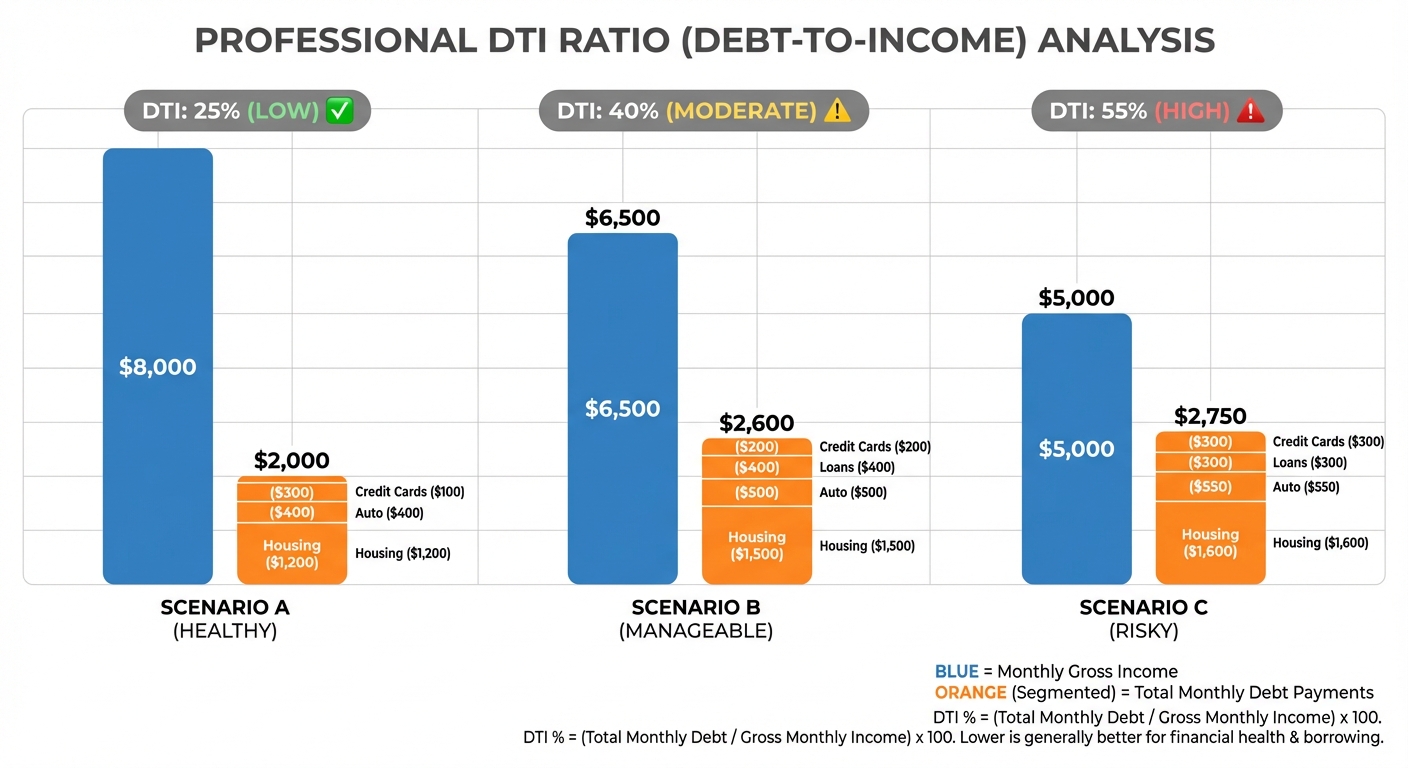

Debt-to-Income Ratio (DTI)

- No more than 43% of your income should go toward the new mortgage payment.

- No more than 49.99% of your income should go toward total monthly debts (mortgage + credit cards + student loans + car loans).

Note: VA and FHA loans can sometimes allow for higher debt ratios on a case-by-case basis.

Employment History

Lenders generally want to see two years of steady employment history, preferably in the same line of work. If you are self-employed, we will look at your tax returns to determine your qualifying income.

Down Payment & Reserves

Buying a Home in Salem, OR with “Less Than Perfect” Credit

Living in Salem offers a wonderful mix of city amenities and access to the beautiful outdoors of the Pacific Northwest. However, the housing market can be competitive. If you are worried that your credit score might hold you back from buying a home in Salem, Keizer, or the surrounding areas, do not disqualify yourself before speaking to a professional.

Local expertise matters. Unlike big box banks or impersonal online lenders, our team understands the local market. We know which loan programs work best for properties in Marion and Polk counties. We can run a Home Purchase Qualifier analysis for you to see exactly where you stand.

If your score isn’t quite there yet, we don’t just say “no.” We help you understand why and offer guidance on what needs to happen to get you to “yes.”

Actionable Tips to Improve Your Credit Score

- Check for Errors: Pull your credit reports from the three major bureaus (Equifax, Experian, TransUnion). If you see errors, dispute them immediately.

- Pay Down Balances: Credit utilization (how much of your limit you are using) is a huge factor. Try to keep credit card balances below 30% of the limit.

- Don’t Close Old Accounts: The length of your credit history matters. Keep those older accounts open, even if you don’t use them often.

- Avoid New Hard Inquiries: Do not apply for a new car loan or credit card right before applying for a mortgage. This can temporarily dip your score.

- Pay Everything on Time: Payment history is the biggest chunk of your score. Set up autopay to ensure you never miss a due date.

Why Choose a Local Broker Over a Big Bank?

When you are trying to figure out financing, you might be tempted to just walk into your local bank branch. However, working with an independent mortgage broker like Mortgage Marketplace LLC offers distinct advantages:

- More Options: We aren’t tied to one bank’s products. We shop dozens of wholesale lenders to find the rate and terms that fit your specific credit profile.

- Speed: We can often get loans fully funded in 30 days or less.

- Personalized Service: You get the cell phone number of your loan officer—Mike, Stacy, Summer, or Jeremy—not a 1-800 number call center.

- Problem Solving: We specialize in finding solutions for complex scenarios that big banks often reject.

Frequently Asked Questions (FAQs)

1. Can I buy a house with a 500 credit score?

It is difficult, but not impossible. FHA loans technically allow scores as low as 500, but they require a 10% down payment instead of the standard 3.5%. Most lenders, however, have “overlays” requiring a minimum of 580. If your score is 500, we recommend working on credit repair strategies first.

2. Does checking my eligibility hurt my credit score?

When you first speak with us for a consultation or a soft pull, it usually doesn’t impact your score. However, a formal mortgage application involves a “hard inquiry,” which may lower your score by a few points temporarily. The benefits of getting pre-approved far outweigh this small, temporary dip.

3. How fast can I raise my credit score to buy a house?

It depends on what is hurting your score. If it is high utilization, paying down a credit card can boost your score in as little as 30 days (once the card issuer reports the new balance). If the issue is missed payments or a bankruptcy, it will take more time to rebuild.

4. Is the credit score I see on Credit Karma the same one lenders use?

Not always. Consumer sites often use a different scoring model (VantageScore) than mortgage lenders (FICO 2, 4, or 5). It is not uncommon for the score a lender pulls to be slightly different from what you see on free apps. We can pull a tri-merge credit report to give you the most accurate view.

5. Do co-signers help if my credit score is low?

Yes! If you have a willing co-borrower with a strong credit score and income (like a spouse or parent), it can help strengthen your application. However, lenders typically use the lowest median credit score among all borrowers on the loan. This means if your score is very poor, a co-signer might not automatically fix the issue, but they can help with income requirements.

Ready to Check Your Options?

Don’t let the fear of a credit score number keep you renting forever. The market in Salem is moving, and rates change daily. Whether you are looking to buy your first home, upgrade to a larger space, or refinance your current loan, we are here to help.

Get your FREE Pre-Approval Letter or Rate Quote today. Find out exactly how much home you can afford.

Contact Mike Gillett and the Team at Mortgage Marketplace LLC

Call us: (503) 210-1480

Email: mike.gillett@p9t630biym.wpdns.site

Click Here to Get Started Now

Compliance & Licensing Information:

Mortgage Marketplace LLC | NMLS #2367229

3723 Fairview Industrial Dr. SE, Suite 190, Salem, OR 97302

Mike Gillett, Mortgage Broker | NMLS #362285

Equal Housing Opportunity. This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements for refinances, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines. Approvals are subject to change without notice based on applicant’s eligibility and market conditions.