Navigating Mortgage Approvals for Oregon Entrepreneurs

Securing a home loan as an entrepreneur in Salem, OR, or anywhere else in the Pacific Northwest requires a strategic approach. Traditional lending often favors W-2 employees with predictable paychecks, leaving business owners to navigate complex underwriting guidelines. However, variable income does not have to be a barrier to homeownership.

At Mortgage Marketplace, we understand that smart business owners maximize their tax deductions. While this strategy lowers your tax liability, it can artificially deflate your qualifying income on paper. To overcome this, self-employed borrowers can leverage several powerful underwriting strategies:

- Strategic Add-Backs: Certain non-cash expenses, like depreciation and depletion, can be added back to your qualifying income.

- Alternative Document Loans: Bank statement programs allow lenders to evaluate cash flow rather than tax returns.

- Flexible Lender Solutions: Working with a broker gives you access to a wider network of wholesale lenders who specialize in entrepreneurial income.

By understanding how underwriters view your business structure, you can position your application for a strong approval.

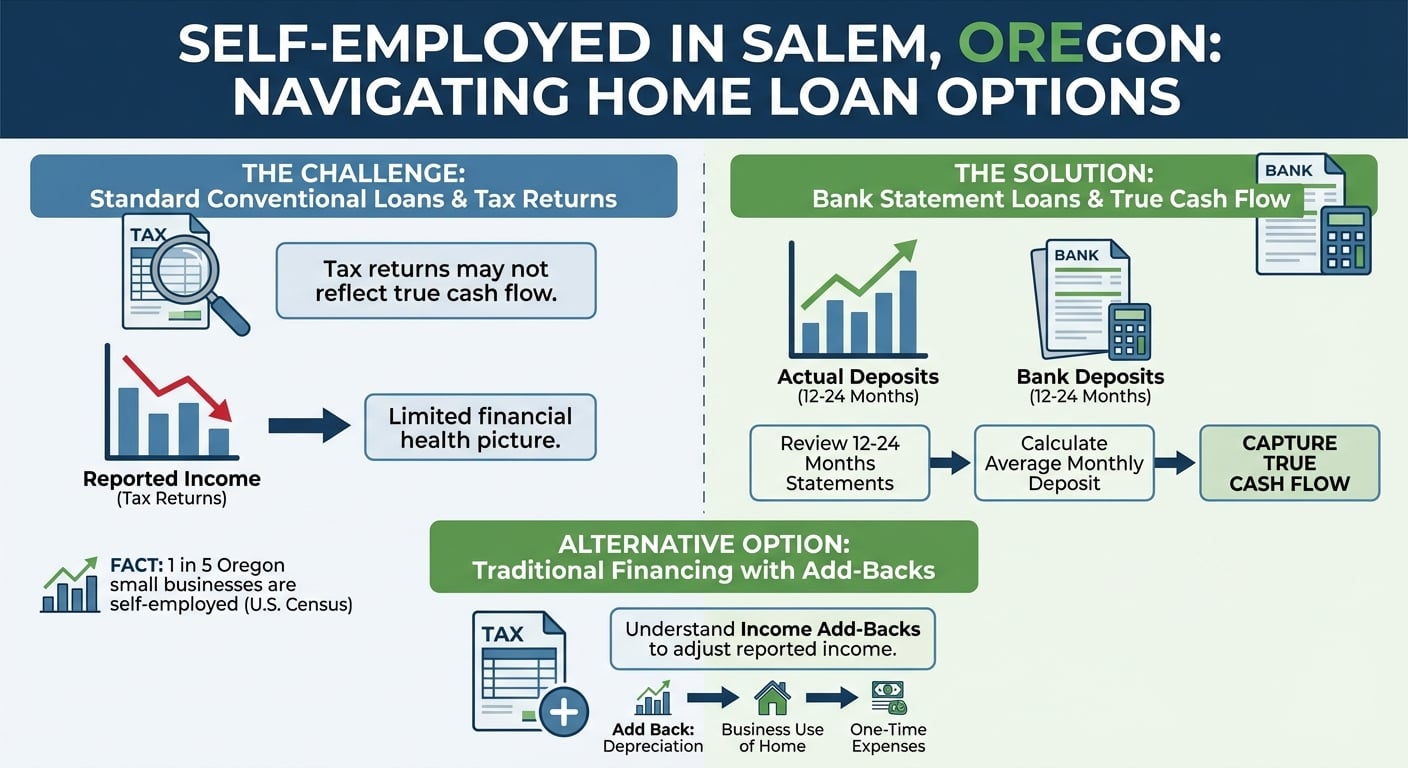

Practical Tactics: Bank Statement Loans and Income Add-Backs

For many self-employed individuals in Salem and the broader Oregon market, standard conventional loans may not paint the full picture of their financial health. This is where Bank Statement Loans become an invaluable tool. Instead of relying on tax returns, underwriters review 12 to 24 months of personal or business bank statements to calculate an average monthly deposit. This method captures your true cash flow.

If you prefer to stick with traditional financing, understanding income add-backs is crucial. Underwriters are permitted to add specific expenses back to your bottom line, boosting your qualifying income. Common add-backs include:

- Depreciation on real estate or equipment

- Amortization of intangible assets

- One-time extraordinary expenses that will not recur

- Business use of home deductions

Our team at Mortgage Marketplace meticulously analyzes your financial profile to determine whether an Alternative Document Home Loan or a traditional path with strategic add-backs is your best route to securing competitive rates.

| Loan Feature | Traditional Financing (Tax Returns) | Bank Statement Loans (Alt-Doc) |

|---|---|---|

| Income Verification | 1 to 2 years of Tax Returns and W-2s/1099s | 12 to 24 months of Bank Statements |

| Impact of Deductions | Lowers qualifying income significantly | No impact; based on gross deposits |

| Ideal Borrower | W-2 employees or low-deduction businesses | Freelancers, contractors, and business owners |

| Down Payment | As low as 3% to 5% | Typically 10% to 20% minimum |

Partnering with Mortgage Marketplace in Salem, OR

Securing the right mortgage structure requires local expertise and access to diverse lending portfolios. As a premier mortgage broker serving Salem, OR, Mortgage Marketplace is dedicated to helping Oregon entrepreneurs achieve their homeownership and investment goals. We offer a clear, efficient path from application to closing.

Whether you are looking to buy a home or explore refinance options, our process is designed to keep things moving smoothly. We compare rate, term, and equity options upfront so your loan can move forward without unnecessary delays.

Compliance Notice: Mortgage Marketplace LLC is an equal housing lender. All loans are subject to underwriting approval. Interest rates and program terms are subject to change without notice.

Ready to review your unique income scenario? Contact Mike Gillett today at 1-503-510-8780 or email mike.gillett@mortgagemarketplace.biz to get started on your customized pre-approval strategy.

Q1: What is a bank statement loan for self-employed borrowers?

A bank statement loan is an alternative documentation program that allows lenders to verify your income using 12 to 24 months of business or personal bank deposits rather than tax returns.

Q2: How long do I need to be self-employed to qualify for a mortgage in Oregon?

Typically, lenders require a two-year history of self-employment. However, some flexible loan programs may allow for just one year if you have previous experience in the same industry.

Q3: Can I use my business funds for a down payment?

Yes, you can use business funds for a down payment, provided you can prove that withdrawing the funds will not negatively impact your business operations. A letter from your CPA or financial professional is often required.

Q4: What are income add-backs in mortgage underwriting?

Income add-backs are non-cash deductions, such as depreciation or one-time business expenses, that underwriters add back to your net income to increase your qualifying income for a mortgage.

Q5: Does Mortgage Marketplace serve borrowers outside of Salem, OR?

Yes, while we are locally focused in Salem, we help home buyers, homeowners, and property investors throughout Oregon access competitive rates and flexible loan programs. Contact Mike Gillett at Mortgage Marketplace Today