Maximizing Your Home’s Value in the Salem Real Estate Market

As we move into 2026, homeowners in Salem, OR and the surrounding Willamette Valley continue to see the value of their properties grow. For many, this accumulated home equity represents a significant financial tool that remains untapped. A cash-out refinance allows you to replace your current mortgage with a new one for a larger amount than what you owe, paying you the difference in a tax-free lump sum of cash.

Whether you are looking to update your kitchen, pay off high-interest credit cards, or invest in a second property, understanding the landscape of refinancing options is crucial. At Mortgage Marketplace LLC, we help local homeowners navigate current interest rates and loan terms to determine if accessing equity is the right strategic move for their financial future.

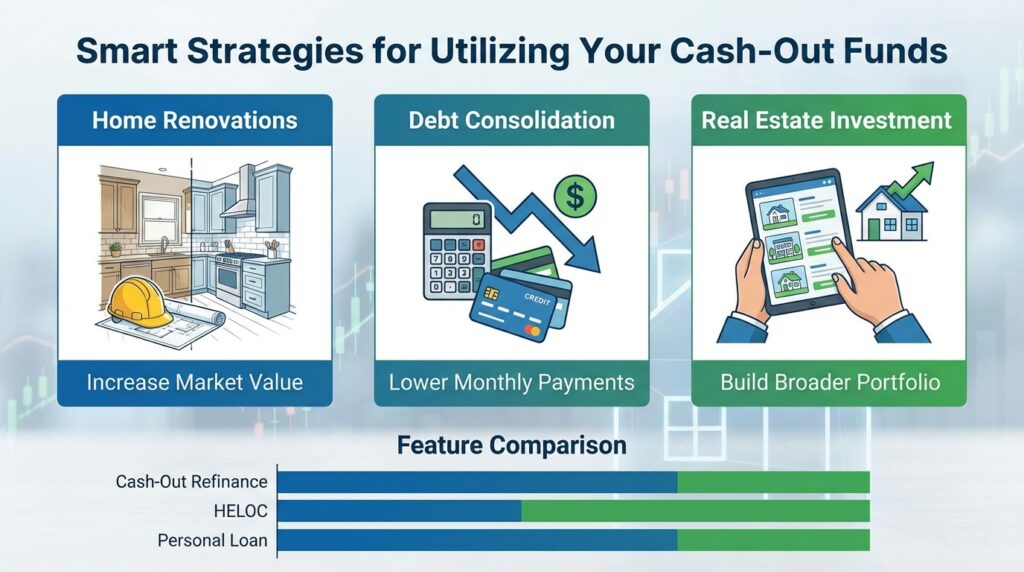

Smart Strategies for Utilizing Your Cash-Out Funds

Once you have unlocked your equity, how you use the funds can have a lasting impact on your net worth. Here are the most common and effective uses for cash-out proceeds in 2026:

- Home Renovations: Reinvesting in your property can increase its market value. Whether it’s adding an ADU (Accessory Dwelling Unit) or modernizing an older Salem home, renovation loans and cash-out options can fund these projects.

- Debt Consolidation: With consumer debt interest rates often far higher than mortgage rates, using equity to pay off credit cards or personal loans can significantly lower your monthly outgoing cash flow.

- Real Estate Investment: savvy homeowners often use their equity as a down payment for an investment property, leveraging their current asset to build a broader portfolio.

It is essential to weigh the long-term costs against the immediate benefits. Consulting with a local expert like Mike Gillett ensures you understand how a new interest rate and loan term will affect your overall financial picture.

| Feature | Cash-Out Refinance | HELOC (Home Equity Line of Credit) | Personal Loan |

|---|---|---|---|

| Interest Rate Type | Typically Fixed | Typically Variable | Fixed (Usually Higher) |

| Closing Costs | Yes (Standard Mortgage Costs) | Lower or None | Minimal to None |

| Tax Deductibility | Yes (If used for home improvements) | Yes (If used for home improvements) | No |

| Repayment Term | 15 to 30 Years | 10 to 20 Years | 3 to 7 Years |

Navigating Qualification and Rates with Local Expertise

To qualify for a cash-out refinance, lenders typically require you to maintain at least 20% equity in your home after the cash is taken out (a maximum Loan-to-Value ratio of 80%). Your credit score and debt-to-income ratio will also play significant roles in determining your interest rate.

Working with a local broker at Mortgage Marketplace LLC offers distinct advantages over big-box lenders. We understand the specific property values in neighborhoods across Salem and Eugene, and we can compare options from multiple lenders to find the specific program that meets your needs—whether that is a Conventional, FHA, or Jumbo loan product. By analyzing your unique scenario, we ensure that refinancing supports your broader goals, rather than just resetting your mortgage clock.

Q1: How much cash can I take out of my home in 2026?

generally, you can borrow up to 80% of your home’s appraised value. For example, if your home is worth $500,000, your new loan amount (including the cash out) cannot exceed $400,000.

Q2: Is the interest on a cash-out refinance tax-deductible?

Interest on the portion of the loan used to buy, build, or substantially improve your home may be tax-deductible. Funds used for debt consolidation or other purchases typically are not. Consult a tax professional for advice.

Q3: Does a cash-out refinance have closing costs?

Yes, similar to your original mortgage, a cash-out refinance involves closing costs such as appraisal fees, title insurance, and origination fees. These can often be rolled into the loan amount.

Q4: How long does the cash-out refinance process take?

In the current market, the process typically takes 30 to 45 days from application to funding, though this can vary based on appraisal availability in the Salem area.

Q5: Can I get a cash-out refinance with an FHA loan?

Yes, FHA loans allow for cash-out refinancing, typically up to 80% of the home’s value, and can be a good option for borrowers with lower credit scores.

Contact Mike Gillett at Mortgage Marketplace LLC today for a free refinance analysis