One of the most persistent myths in the real estate world is that you need a 20% down payment to buy a home. For many aspiring homeowners in Salem, OR, and across the Pacific Northwest, this misconception creates a mental barrier, making the dream of homeownership feel financially out of reach.

The reality? You likely need far less than you think. In fact, many buyers purchase homes with as little as 3% or even 0% down. Whether you are a first-time homebuyer looking at a starter home in Eugene or upgrading to a larger property in Salem, understanding the true requirements can accelerate your timeline to getting the keys.

At Mortgage Marketplace LLC, we believe in empowering our clients with the facts. Led by Michael Gillett, our team is dedicated to finding the loan program that fits your budget and lifestyle. In this guide, we will break down exactly how much cash you really need to buy a house and explore the loan options available to you.

Debunking the 20% Down Payment Myth

Where did the “20% rule” come from? It stems from the threshold required to avoid Private Mortgage Insurance (PMI) on conventional loans. While putting 20% down is excellent for lowering your monthly payments and avoiding PMI, it is not a requirement to obtain a mortgage.

In today’s market, waiting years to save 20% of a purchase price—which could be upwards of $80,000 to $100,000 depending on the property—often means missing out on appreciation and building equity. Modern loan programs are designed to help you enter the market sooner with much lower upfront costs.

Down Payment Requirements by Loan Type

The amount you need for a down payment depends entirely on the type of mortgage loan you choose. Different government-backed and conventional programs have different minimums. Here is a breakdown of the most common loan types we offer at Mortgage Marketplace LLC:

1. Conventional Loans (3% to 5% Down)

Conventional loans are not insured by the federal government, but they follow guidelines set by Fannie Mae and Freddie Mac. They are a popular choice for buyers with good credit scores.

- First-Time Home Buyers: Qualifying first-time buyers can put down as little as 3%.

- Repeat Buyers: Typically require a minimum of 5% down.

If you put down less than 20%, you will typically pay PMI, but this can be removed once you reach 20% equity in your home. To see if this is the right fit for you, explore our Loan Options.

2. FHA Loans (3.5% Down)

Insured by the Federal Housing Administration, FHA Loans are fantastic for buyers who may have lower credit scores or higher debt-to-income ratios. The minimum down payment is fixed at 3.5% for borrowers with a credit score of 580 or higher.

This is often the “go-to” loan for first-time buyers in Salem who want a low down payment option with flexible qualification standards.

3. VA Loans (0% Down)

If you are a veteran, active-duty service member, or a qualifying surviving spouse, the VA Loan is arguably the best mortgage product available. It allows for 0% down payment.

Additionally, VA loans do not require monthly mortgage insurance (PMI), even with zero money down. This can save you hundreds of dollars a month compared to other loan types.

4. USDA Loans (0% Down)

The U.S. Department of Agriculture offers loans to encourage homeownership in rural and suburban areas. Many areas surrounding Salem and Eugene, OR, qualify for USDA Loans.

Like VA loans, USDA loans offer 100% financing (0% down) for qualified properties and borrowers who meet specific income limits.

5. Jumbo Loans (10% to 20% Down)

If you are buying a luxury home that exceeds the conforming loan limits, you may need a Jumbo Loan. Because these loans carry higher risk for lenders, they typically require a larger down payment, often between 10% and 20%, along with a strong credit history.

Comparison: Minimum Down Payment by Loan Type

Here is a quick reference guide to help you compare your options:

| Loan Type | Minimum Down Payment | Ideal For |

|---|---|---|

| VA Loan | 0% | Veterans and active military members. |

| USDA Loan | 0% | Buyers in rural/suburban areas with low-to-moderate income. |

| Conventional (First-Time) | 3% | Buyers with good credit (620+) buying their first home. |

| FHA Loan | 3.5% | Buyers with lower credit scores or higher debt. |

| Conventional (Standard) | 5% | Repeat buyers with good credit profiles. |

| Jumbo Loan | 10-20% (Varies) | High-value properties exceeding conforming limits. |

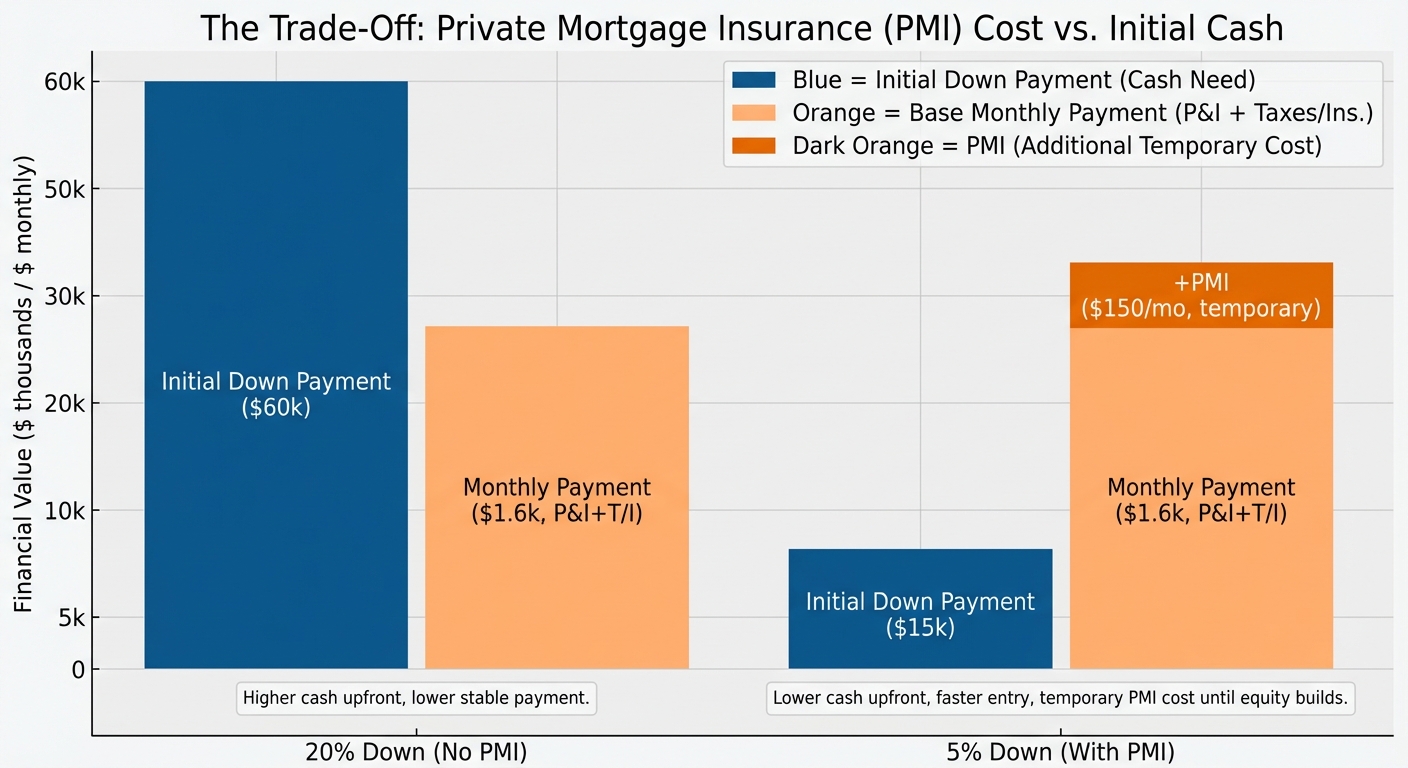

The Trade-Off: Private Mortgage Insurance (PMI)

- PMI (Conventional): Can be cancelled once you reach 20% equity.

- MIP (FHA): Mortgage Insurance Premiums on FHA loans usually last for the life of the loan if you put down less than 10%.

- Funding Fees (VA/USDA): While they don’t have monthly PMI, VA and USDA loans often have upfront guarantee fees that can be rolled into the loan amount.

Even with these costs, buying now with a low down payment is often smarter than paying rent for another five years while trying to save for a 20% down payment. You can use our Mortgage Calculator to see how different down payment amounts affect your monthly payment.

Closing Costs: The Hidden Expense

When budgeting for your home purchase in Salem, remember that your down payment isn’t the only upfront cost. You also need to budget for closing costs.

Closing costs typically range from 2% to 5% of the loan amount. These cover appraisal fees, title insurance, origination fees, and prepaid taxes/insurance. In some cases, we can help you negotiate with the seller to cover a portion of these costs, or use specific loan programs that allow for closing cost assistance.

Buying a Home in Salem, OR: Local Insights

The real estate market in Salem and the broader Willamette Valley is dynamic. Prices have fluctuated, and inventory changes quickly. Working with a local expert like Mike Gillett and the team at Mortgage Marketplace LLC offers distinct advantages over big-box online lenders.

- Local Knowledge: We understand the specific property types in Oregon, from manufactured homes to rural estates eligible for USDA financing.

- Competitive Pre-Approval: In a competitive market, a generic pre-qualification letter isn’t enough. Our Home Purchase Qualifier provides a robust pre-approval that shows sellers you are a serious, qualified buyer.

- Personalized Service: We are located right here at 3723 Fairview Industrial Dr. SE, Suite 190, Salem, OR 97302. You can meet us face-to-face or via Zoom.

Can I Use Gift Funds for My Down Payment?

Yes! This is a common strategy for first-time buyers. Most loan programs allow family members to “gift” you the money for your down payment. However, this must be a true gift, not a loan disguised as a gift. We will help you document the paper trail properly to ensure the underwriter accepts the funds.

5 Frequently Asked Questions About Down Payments

1. Is it better to put down 20% if I have it?

2. Can I borrow money for a down payment?

Typically, you cannot take out a personal loan (like a credit card advance or unsecured bank loan) to pay for your down payment because it increases your debt-to-income ratio. However, there are specific Down Payment Assistance (DPA) programs and second mortgages designed specifically for this purpose. Contact us to see if you qualify for any Oregon-specific assistance.

3. Does a higher down payment get me a better interest rate?

Yes, usually. Lenders view a larger down payment as a sign of financial stability and lower risk. Consequently, they often offer lower interest rates to borrowers who put more money down. You can check current scenarios with our Refinance Rate Checker or purchase quote tools.

4. What is “Earnest Money” and is it part of the down payment?

Earnest money is a “good faith” deposit you make when your offer on a house is accepted (usually 1% to 2% of the purchase price). The good news is that this money is credited toward your down payment and closing costs at the closing table. It is not an extra fee; it is essentially a prepayment of your down payment.

5. How do I prove where my down payment came from?

Lenders are required to verify the source of your funds to prevent money laundering. You will typically need to provide 60 days of bank statements. If there are large, unexplained deposits, you will need to provide a letter of explanation. We guide you through this process to ensure your documentation is perfect.

Ready to Find Out What You Qualify For?

Don’t let the fear of a large down payment stop you from building wealth through real estate. Whether you have 3%, 20%, or qualify for a 0% down program, Mortgage Marketplace LLC is here to help you navigate the process in Salem, Eugene, and throughout Oregon.

Every homebuyer’s financial situation is unique. Let’s run the numbers together and find the loan that fits your life.

Get Your FREE Personalized Rate Quote Today!

Call us at (503) 210-1480 or email mike.gillett@p9t630biym.wpdns.site.

Mortgage Marketplace LLC

NMLS #2367229

3723 Fairview Industrial Dr. SE, Suite 190

Salem, OR 97302

(503) 210-1480

This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements for refinances, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines. Approvals are subject to change without notice based on applicant’s eligibility and market conditions. Mortgage Marketplace, LLC. NMLS #2367229 is an Equal Housing Opportunity.