Buying a home is one of the most significant financial milestones in your life. Whether you are looking at a charming bungalow in downtown Salem, a family home in Eugene, or a rural property in the outskirts of Marion County, the excitement of house hunting often starts with a dream. However, before you start scrolling through listings or attending open houses, you need to answer the most critical question: “How much house can I afford?”

At Mortgage Marketplace LLC, we believe that financial clarity is the foundation of a happy home. Led by Mike Gillett and our experienced team in Salem, OR, we are dedicated to helping you navigate the complex world of mortgage financing. This guide will break down the factors that determine your purchasing power, explain the nuances of debt-to-income ratios, and show you how to maximize your budget in today’s Oregon real estate market.

The Golden Rule of Affordability: Understanding DTI

When lenders determine how much money they are willing to lend you, they don’t just look at your salary. The most important metric we use is the Debt-to-Income (DTI) ratio. This ratio compares your gross monthly income (before taxes) to your monthly debt obligations.

There are typically two types of ratios lenders analyze:

- The Front-End Ratio: This is the percentage of your annual gross income that goes toward paying your mortgage (principal, interest, taxes, and insurance). Ideally, lenders prefer this to be around 28%, though many programs allow for higher percentages.

- The Back-End Ratio: This includes your mortgage payment plus all other monthly debts, such as credit card payments, car loans, and student loans.

- The 43/49 Rule: Generally, qualified mortgages require a DTI of 43% or lower. However, at Mortgage Marketplace, we have access to loan programs (like FHA and VA loans) that may allow for a total debt ratio up to 49.99% or even higher on a case-by-case basis.

Understanding your DTI is crucial because it directly impacts your loan eligibility and the interest rate you may qualify for.

Key Factors Influencing Your Home Buying Budget

While your income is the starting point, several other levers move the needle on your affordability. Here is what you need to know to determine your true budget.

1. Your Credit Score

Your credit score is a snapshot of your financial reliability. A higher score signals to lenders that you are a lower risk, which often translates to a lower interest rate. Even a fraction of a percentage point difference in your interest rate can save—or cost—you tens of thousands of dollars over the life of a 30-year loan.

If your credit score is lower than you’d like, don’t panic. We specialize in helping borrowers with various credit profiles. Whether you have excellent credit or are working to rebuild it, we can help you explore options like FHA Loans which are more forgiving regarding credit history.

2. The Down Payment

A common myth is that you need a 20% down payment to buy a home. While putting 20% down helps you avoid Private Mortgage Insurance (PMI), it is not a requirement for most buyers in Salem and throughout Oregon.

- Conventional Loans: Often require as little as 3% to 5% down.

- FHA Loans: Require a minimum of 3.5% down.

- VA Loans: Offer 0% down payment options for eligible veterans and active-duty military.

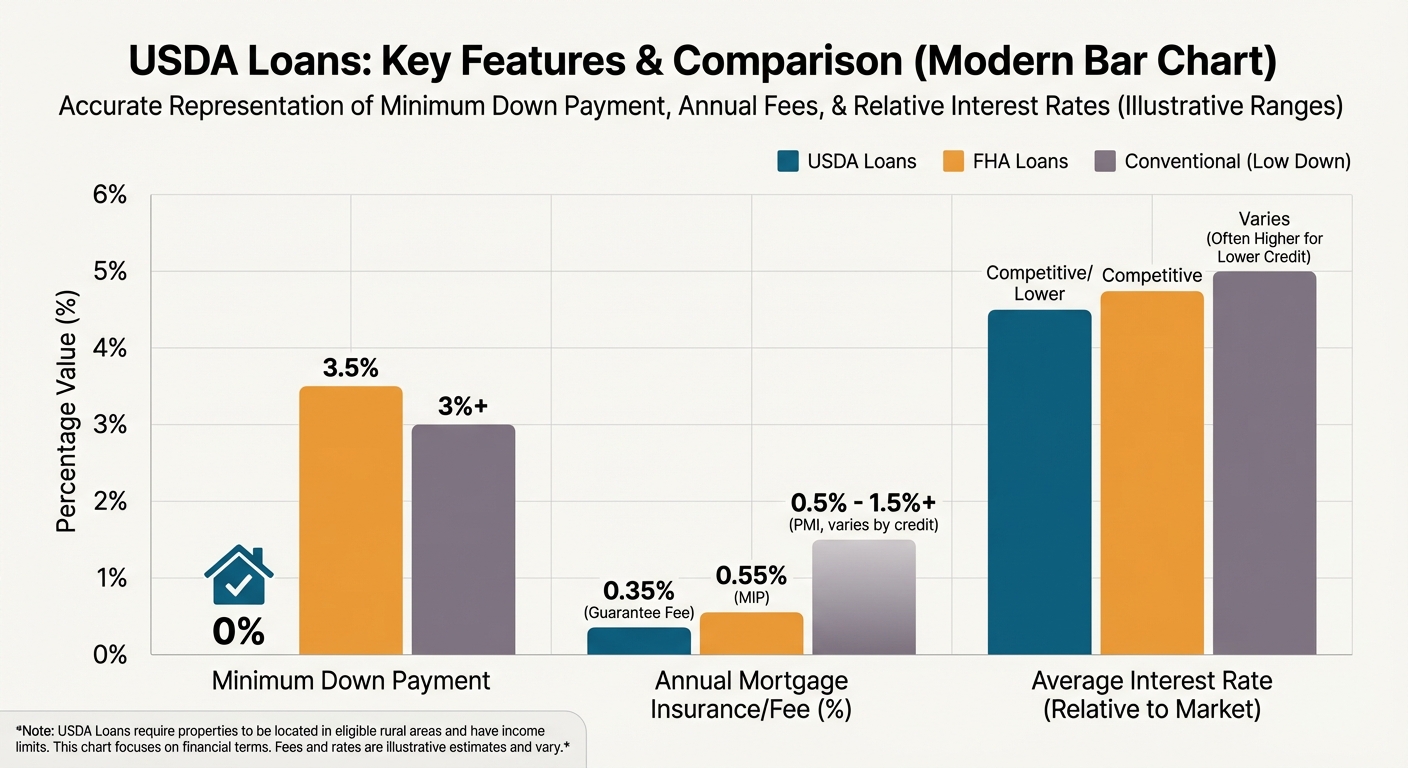

- USDA Loans: Offer 0% down payment for homes in eligible rural areas.

If you are struggling to save for a down payment, ask us about Down Payment Assistance programs that might be available to you.

3. Interest Rates

Interest rates are fluid and change daily based on economic factors. When rates are low, your purchasing power increases because your monthly payment is lower for the same loan amount. Conversely, when rates rise, your purchasing power decreases. Checking Today’s Rates is a good way to gauge the current market, but locking in a rate with a pre-approval is the only way to secure it.

The Hidden Costs of Homeownership in Oregon

When calculating “how much house can I afford,” many online calculators only look at Principal and Interest. However, a responsible budget must include the “PITI” plus other costs:

- Principal: The money paying down the loan balance.

- Interest: The cost of borrowing the money.

- Taxes: Property taxes in Oregon vary by county. In Marion County (Salem area), property taxes can significantly add to your monthly obligation.

- Insurance: Homeowners insurance protects your asset against fire, theft, and liability.

- HOA Fees: If you are buying a condo or a home in a planned community, Homeowners Association (HOA) fees must be factored into your DTI.

- Maintenance: We recommend budgeting 1% of the home’s value annually for repairs and maintenance.

Loan Programs and Your Budget

Different loan programs have different affordability calculations. Choosing the right loan product is just as important as finding the right house.

FHA Loans

Backed by the Federal Housing Administration, FHA loans are fantastic for first-time buyers. They allow for lower credit scores and a down payment of just 3.5%. Because the underwriting guidelines are more flexible, you might qualify for “more house” with an FHA loan than a strict conventional loan.

VA Loans

If you are a veteran, active-duty service member, or a surviving spouse, the VA loan is likely your best option. With $0 down payment required and no monthly mortgage insurance, your monthly payment goes further toward the principal, increasing your purchasing power.

USDA Loans

For those looking to buy in rural areas surrounding Salem or Eugene, USDA loans offer 100% financing (no down payment). Income limits apply, but this is an excellent tool for affordability in designated rural zones.

Jumbo Loans

If you are looking at luxury properties that exceed the conforming loan limits (which change annually), you will need a Jumbo Loan. These typically require higher credit scores and larger down payments, but Mortgage Marketplace offers competitive terms for high-value real estate.

Affordability Scenarios: A Comparison

To help you visualize how interest rates and down payments affect what you can afford, consider the following hypothetical scenarios. (Note: These figures are for educational purposes only. Taxes and insurance are estimates.)

| Scenario | Home Price | Down Payment | Loan Amount | Interest Rate (Est.) | Monthly Principal & Interest |

|---|---|---|---|---|---|

| Scenario A | $400,000 | 3.5% ($14,000) | $386,000 | 6.5% | $2,440 |

| Scenario B | $400,000 | 20% ($80,000) | $320,000 | 6.5% | $2,023 |

| Scenario C | $450,000 | 10% ($45,000) | $405,000 | 6.0% | $2,428 |

As you can see, a larger down payment or a slightly lower interest rate can significantly impact your monthly payment, or allow you to purchase a more expensive home for the same monthly cost. Using our Mortgage Calculator can help you run these numbers based on your specific situation.

The Importance of Local Expertise in Salem, OR

Real estate is hyper-local. What applies to the national market doesn’t always apply to Salem, Eugene, or the Willamette Valley. Working with a local mortgage broker like Mike Gillett and the team at Mortgage Marketplace gives you a distinct advantage.

We understand the local property tax rates in Marion, Polk, and Lane counties. We know which condo developments are FHA-approved. Most importantly, local real estate agents know us. When you submit an offer with a Pre-Approval Letter from a reputable local lender, it carries more weight than a generic letter from a big-box online bank. Sellers want to know the deal will close, and our reputation in Salem ensures confidence.

Pre-Qualification vs. Pre-Approval

To truly know what you can afford—and to be taken seriously by sellers—you need a Pre-Approval. This involves:

- Pulling your credit report.

- Verifying your income (pay stubs, W2s, tax returns).

- Verifying your assets (bank statements).

- Running your file through an Automated Underwriting System (AUS).

Once pre-approved, you are essentially a cash buyer in the eyes of the seller, subject only to the property appraisal and title work. You can start the process today with our Home Purchase Qualifier.

5 Tips to Increase Your Home Affordability

If the numbers aren’t quite adding up to the home you want, here are five actionable steps to boost your budget:

- Pay Down Consumer Debt: Lowering your credit card balances or paying off a car loan improves your DTI ratio immediately.

- Boost Your Credit Score: Correct errors on your credit report and keep credit card utilization below 30%.

- Consider a Co-Borrower: Adding a spouse or family member to the loan adds their income to the calculation (but also their debts and credit score).

- Look for Lower PMI: Conventional loans with high credit scores have cheaper mortgage insurance than FHA loans in some cases. We can compare both for you.

- Buy Down the Rate: You can pay “points” upfront to lower your interest rate, reducing your monthly payment permanently.

Frequently Asked Questions (FAQs)

1. How much income do I need to buy a $400,000 house in Salem, OR?

This depends heavily on your down payment, interest rate, and other debts. Generally, lenders look for a housing payment that is roughly 28-31% of your gross monthly income. Assuming a moderate interest rate and average property taxes, a household income between $85,000 and $100,000 is often a good starting benchmark, but this varies wildly based on your specific debt profile.

2. Can I use gift money for my down payment?

Yes! Most loan programs, including FHA and Conventional loans, allow you to use gift funds from family members for your down payment and closing costs. We can provide you with a specific “gift letter” template to document the transfer of funds properly.

3. Does checking my affordability hurt my credit score?

Using our online calculators or speaking with us for an initial consultation does not hurt your score. However, when you move to the official Pre-Approval stage, we will need to do a “hard pull” on your credit. This may lower your score by a few points temporarily, but it is a necessary step to get a mortgage.

4. What if I have changed jobs recently?

Job stability is key, but changing jobs doesn’t automatically disqualify you. If you stayed in the same line of work or moved for a higher salary, lenders often view this positively. Gaps in employment or switching from a salaried job to commission-only work can be more complex and require more documentation.

5. Should I wait for interest rates to drop before buying?

Trying to time the market is risky. While you wait for rates to drop, home prices in Salem may continue to rise, negating the savings. Remember the saying: “Marry the house, date the rate.” You can always refinance later if rates drop significantly, but you cannot go back and buy a house at last year’s price.

Ready to Find Your Dream Home?

Determining “how much house can I afford” is not just about plugging numbers into a calculator; it is about building a strategy for your financial future. At Mortgage Marketplace, we are committed to providing you with transparent, personalized advice to get you into the right home with a loan you can comfortably afford.

Don’t guess with your financial future. Let our team in Salem, OR, provide you with a custom analysis.

Contact Mike Gillett and the team today:

Phone: (503) 210-1480

Email: mike.gillett@p9t630biym.wpdns.site

Location: 3723 Fairview Industrial Dr. SE, Suite 190, Salem, OR 97302

CLICK HERE TO GET YOUR FREE PRE-APPROVAL LETTER NOW

Mortgage Marketplace LLC | NMLS #2367229

Mike Gillett | NMLS #362285

Equal Housing Opportunity.

This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements for refinances, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines.